Alright, let’s dive into the world of mortgages and the Mortgage Number tool in more detail.

Buying a home is a big financial decision, and for most people, it involves getting a mortgage loan. A mortgage is a loan that is used to purchase a property, and it is typically paid back over a period of 15 to 30 years. In order to get a mortgage, borrowers need to meet certain financial requirements, and one of the most important factors that lenders consider when reviewing a mortgage application is the borrower’s financial situation. Mortgage defined, click here.

That’s where the Mortgage Number tool comes in. It’s a tool designed to help borrowers understand their financial strengths and weaknesses before they apply for a mortgage. Mortgage Number provides borrowers with a numerical representation of their overall financial situation with transparency, which can be used to assess their eligibility for a mortgage loan and secure favorable mortgage terms. Mortgage Number is NOT a credit score. A credit score is just one variable out of seven that makes up your Mortgage Number; Mortgage Number is more advanced.

So, how does Mortgage Number make a Mortgage Number?

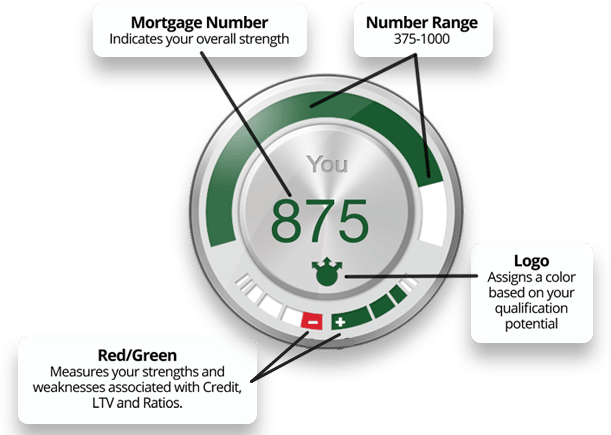

We take into account multiple variables that are weighted around importance through our algorithm that provides a number between 375-1000 or where one fits into today’s lending environment. Here is an area to research more about the Mortgage Number platform; https://mortgagenumber.com/research/.

Increase your chances of approval with confidence! Let’s take a look.

Confidence in your Mortgage Number

Confidence in your Mortgage Number

Credit Score:

One of the most important factors that lenders consider when reviewing a mortgage application is the borrower’s credit. It is used to assess the borrower’s ability to manage debt. Mortgage Number takes into account a borrower’s credit score, which is a numerical representation of their creditworthiness. The higher the credit score, the more likely a borrower is to qualify for a mortgage loan and receive favorable terms.

Debt-to-Income Ratio:

Another important factor that lenders consider when reviewing a mortgage application is the borrower’s debt-to-income ratio. This is a measure of how much debt a borrower has compared to their income. Mortgage Number takes into account a borrower’s debt-to-income ratio and can alert borrowers that they may need to reduce their debt before applying for a mortgage.

Down Payment Amount, LTV:

The down payment amount is the amount of money that a borrower puts down when purchasing a property. Mortgage Number takes into account a borrower’s down payment amount and can indicate whether they are likely to be approved for a mortgage. Generally speaking, the more money a borrower puts down, the less risky they are to the lender, and the more likely they are to receive favorable mortgage terms.

Income:

Your income is the engine behind what you can qualify for or not. You may have perfect credit but NO income. and cannot qualify for a loan.

Overall Financial Situation:

Finally, Mortgage Number takes into account a range of other financial factors, such as outstanding debts, income level, and overall financial stability, ratios. By analyzing all of these factors, Mortgage Number provides borrowers with a comprehensive assessment of their financial situation. This invaluable tool can be used to assess a potential homeowner’s eligibility for a mortgage loan and secure favorable mortgage terms.

So, how can borrowers use the Mortgage Number tool to their advantage?

Borrowers can get a sense of their financial situation by using Mortgage Number before applying for a mortgage. For example, if a borrower’s credit score is low, they may need to work on improving their credit. Similarly, if a borrower’s debt-to-income ratio is high, they may need to pay down some debt. Mortgage Number provides transparency to where you can actually see what Mortgage Number is through our number and dial.

In addition to credit score and debt-to-income ratio, lenders look at other financial factors like the down payment amount and outstanding debts. Mortgage Number takes all of these factors into account and provides borrowers with a comprehensive assessment of their financial situation. Analyzing these factors, Mortgage Number generates a numerical representation of a borrower’s ability to qualify for a mortgage loan. This can range from 375 to 1000, with 1000 being the best outcome.

Mortgage Number 1000 can determine if a borrower is overqualified for a mortgage loan, which is a good thing! Additionally, it can provide borrowers with this comprehensive view of their financial situation, Mortgage Number can help. We help borrowers understand their strengths and weaknesses and take steps to improve their ability or reach! Give it a spin! https://mortgagenumber.com

It Can Be Confusing, But Not Any More!

It Can Be Confusing, But Not Any More! We made it simple.

We made it simple.