How do I calculate minimum monthly Debt?

It is critical you get your minimum monthly Debt number right and hope this provides information that is useful to help you scale your mortgage goals and save you time. Ideally having no monthly debt should be the goal as you can stretch your dollars much further and qualify for more, it gives you more options is all.

What counts?

Calculating your minimum monthly debt can be a real pain in the assets. But don’t worry, we’re here to help!

To start, let’s clarify what counts as debt. If it shows up on your credit report, like personal loan, car payment or credit card bills, then it counts. Let’s not forget about alimony if there is, But if you owe money to your cousin for that time they bailed you out of jail, then that doesn’t count (sorry, cuz).

So, let’s re-cap

Say you have 3 credit cards, a car payment and a loan, could be a personal or student loan.

Credit card #1 balance is, say $1,200 and the minimum monthly payment is $50.00. Credit card #2 balance is $800 and the minimum monthly payment is $35.00. Credit card #3 balance is $600 and the minimum monthly is $25.00. Your car payment is $447 per month and your personal or student loan is $336 per month. It sounds like you’re in more debt than the US government, but don’t panic just yet. We just need to figure out your minimum monthly debt payment.

Here’s an underwriting hack for you: if you have less than 10 months left on a car, boat, RV, or personal/student loan, you don’t need to count those payments. It’s like a get-out-of-debt-free card, but with a time limit.

So, what’s the magic number that the bank underwriter will use? Drumroll please… it’s $893. If that number makes you want to curl up in the fetal position, don’t worry, you’re not alone.

Debt is an uphill battle

But here’s the good news: if you didn’t have that pesky debt, you could qualify for a mortgage while making $2,232 less per month. That’s like winning the lottery, but without all the screaming and confetti. What does this mean? Without that Debt you could qualify making $2,232 less per month, but you need to make $2,232 MORE per month because of the $893 monthly minimum debt payment with the same loan amount.

To help you figure out your finances, check out Mortgage Number’s awesome calculations. They have everything from “Income to Qualify” to “Borrowing Power” to “Rent Money” (which is not to be confused with the money you spend on rent boys and girls, that’s a different blog post entirely). They even have a payment calculator that can help you find the fourth missing number. It’s like playing a game of math Sudoku, but without all the anxiety and pencil marks.

In conclusion, debt sucks. But with a little bit of humor and some helpful calculations, you can figure out your minimum monthly debt and take control of your finances. And who knows, maybe one day you’ll be debt-free and able to afford that yacht you’ve always wanted. (Just don’t forget to invite us on your maiden voyage!)

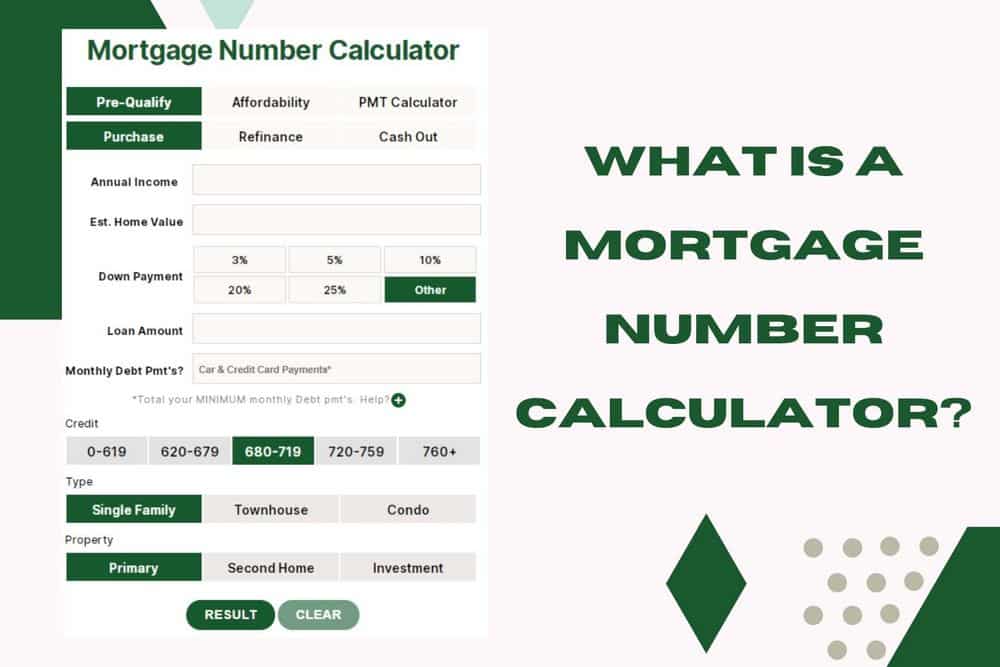

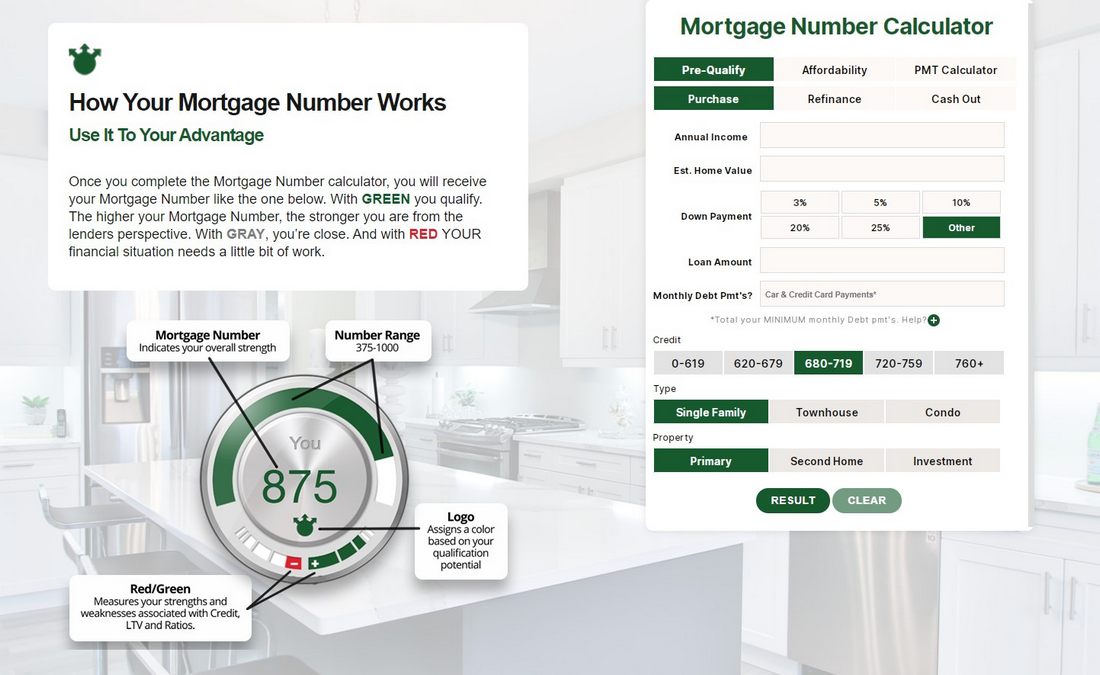

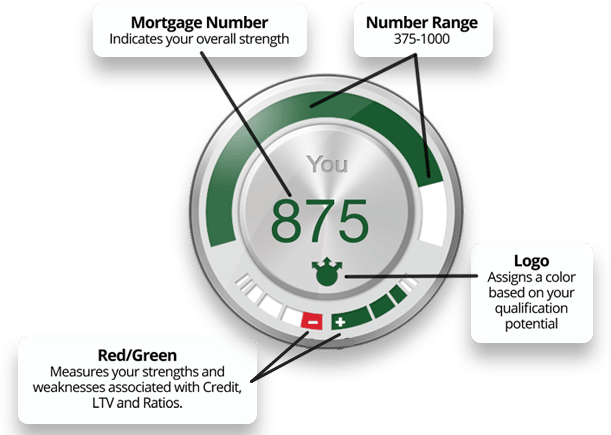

Get your mortgage number today, it’s easy!

It Can Be Confusing, But Not Any More!

It Can Be Confusing, But Not Any More! We made it simple.

We made it simple.