Mortgage Qualification Made Simple

Get your Mortgage Number

And Pre-Qualify With Confidence

See for yourself…

![]()

Get Your Mortgage Number

|

Pre-Qualify

Affordability

PMT Calculator

|

|||

| Total Principal Paid: | |||

| Total Interest Paid: | |||

| Total Amount Paid: | |||

| Extra Monthly PMT: | |||

| Interest Saved: | |||

| Months Saved: | |||

| Zero Balance Date: |

|

||

| Years From Now: | |||

| New Payment: | |||

Helpful Terms & Info:

Minimum Monthly Debt Payment

Add up any car payment(s), student loan(s) payments and credit card, ‘minimum’ payment(s) in this field. It is important to get this number right!

Questions

1. Do you have Credit Card Debt?

2. Do you have Car payments?

3. Do you have Student loans and/ora personal loan?

Answers

1. Add up the Minimum credit card payment(s) the credit card holder is asking for per month. $0.00

2. Add up the Car payment(s). $0.00

3. Add up the loan payment(s). $0.00

Annual Income

W2 EMPLOYEEEnter your “Gross” annual income in this field.

SELF-EMPLOYED

Enter your “Net” annual income in this field.

Trouble can come from Self Employed individuals as deductions can reduce qualifying ability. Basically, reporting less income by paying less in taxes can hurt qualifying.

NON-QM LOANS

Qualified Mortgages were born from the financial situation we found ourselves in after 2007. These new rules over regulated the mortgage sector. Now with Non-QM loans there are ‘Bank statement loans’ that resemble what the limited documentation (EZ Doc) loans were and can make the difference in qualifying!

You would need 12-24 months of bank statements averaging the deposits over that time period to determine your monthly income. It works! Perfect fit for self-employed borrowers who are unable to document income with tax returns.

Alimony & Child Support

Either one or both must be added in the Debt field if you are paying alimony and/or child support. If you’re receiving alimony you can add this to your income but not the child support amount.

Loan Amount

This is the amount that the Bank or Lender will lend to you.

Purchase Price

This can have two meanings:

1) The amount the seller wants for the home AND what the bank believes is the true value of said property are both equal, so it’s best for you to have the home appraise for the price or higher!

2) What the seller wants for the home BUT the bank believes the true Value of said property is less. In this situation, to get financing you must bring the difference of the amount between the seller’s asking price and what the bank believes is the value.

For example: Seller’s asking price is $400,000, but the bank’s appraiser values the home at $380,000. You would therefore need to come in with $20,000, the difference between the two amounts – IN ADDITION to the down payment required by the lender.

Value

On a refinance or Cash Out refinance the value is equal to what the appraised value is. That amount is what the lender will lend on based on their underwriting guidelines and Loan To Value (LTV) ratios.

Example, if the purchase price or value of a said property is $200,000 and the loan amount is $160,000, the LTV is 80% ($160,000 divided by $200,000, it’s the lowest number divided by the larger number for %. ;).

LTV & CLTV

Ratios of value and loan(s). Loan To Value and Combined Loan To Value. This is when you might have a second loan or HELOC (Home Equity Line Of Credit) behind your first loan or mortgage.

Using the numbers above, a first loan of $160,000 and say a HELOC of $20,000 with the value of $200,000 would be viewed as an 80% LTV and a 90% CLTV.

HELOC

Home Equity Line Of Credit. It’s not a second even though a HELOC is behind the first mortgage/loan. A HELOC is like a credit card, you pay based on your balance.

Monthly debt pmt’s

Simply add up all minimum monthly payments from credit card(s), auto loan(s) payment(s), personal loans, student loans, etc. Add these up for a monthly total and entered into the field.

DO NOT include cell phone, water, electric or any other monthly household bills. Also, DO NOT include mortgage payments, property taxes or insurance payments in this field.

Property Tax, Insurance & Misc.

Both the Property Tax and Insurance amounts are estimated. Only you can know these amounts. It would be in your best interest to enter the proper amounts for a better result. These fields are found on the Result page in Advanced.

There is another field, Misc. available for any additional monthly cost associated with the said property like HOA, additional tax or other. Any amount entered here will be included in the “PITI” or “ITI” (Interest Only, Tax and Ins.) totals.

PITI—what is that again?

Principle, interest, taxes and insurance. You would also include HOA fees and PMI (private mortgage insurance) in that number, if relevant.

So, for example, if you have a maximum amount of $1,837 a month of PITI, then ALL of the principle, interest, taxes (property) and interest + HOA and PMI can not exceed that maximum number.

Down payment

Lenders tend to like “20% down” but that’s not to say you can’t put 15%, 10% or 5% down, or anything in-between, up to certain loan amounts. If you’re putting less than 20% down, lenders require PMI.

PMI

Private Mortgage Insurance is when you put less that 20% down on your home. However, some lenders will ‘bake’ that premium into a high interest rate, thus not concerning PMI.

Private mortgage insurance is typically based on a percent of your loan amount, for example, .008 times a loan amount of $250,000 = $2,000. Divide that by 12, and you’ll find that $166 is your monthly premium.

However, some lenders will ‘bake’ that premium into a high interest rate, thus not concerning PMI.

So how can you get rid of PMI? If the value goes up, you refi into another loan, and enough time passes you can petition the lender to remove it, which is not a fun process. And if the premium is baked into the interest rate, you’re simply not going to remove it; your rate is your rate.

Moreover, PMI is insurance in case you default on the loan. The insurance company takes that risk up to 20%, and not the lender. The lender has to step in above the 20% level.

Ratios

Traditionally, lenders use 28% front-end and 36% back-end for ratios. What does that mean?Let’s say you make $10,000 per month. In this case, 28% would equal $2,800 per month that the lender would allow you to use for PITI. The 36% or $3,600 in this example is your PITI plus your monthly debt payments. In this case, that’s up to $1,200 in reoccurring debt.

These are loose guidelines and not set in stone. Lenders will take into account a number of compensating factors—great credit, lots of money in the bank, lots of equity in the home and the current lending environment can all make a difference from lender to lender. Our model is more progressive and grounded in today’s lending realities, so don’t sell yourself short with traditional ratios because things are different today.

Affordability—Income to Qualify

Enter your annual income and your monthly debt payments, add up your minimum credit card payments along with car payments and any other personal loans (i.e., student loans). Then select the term, 30 year or 15 year. Remember, you’ll need more income for a 15-year loan because your payment is higher, due to the shorter term of the loan.

What you’ll see displayed is the monthly and yearly income necessary to qualify, based on your income, monthly debt amount and the interest rate of the day. Toggle your debt amount downwards and you’ll see that with less debt, your “income needed” decreases, because with less debt you need less income to qualify. You can also adjust the interest rate that changes your income requirements.

Note: the amount you qualify for has been reduced by a factor that accounts for monthly property tax and insurance amounts. This number is more realistic than not reducing that amount. For the most accuracy, go to the Result page and adjust these numbers in the Advanced area or at the Home page.

Affordability – Borrowing Power

This feature displays how much you can borrow or finance based on your annual income and Debts. Kind of reverse of the ‘Income to Qualify’ button. Here displays the Amount of a loan you can qualify for based on your Income and Debt. This is based on the maximum PITI amount per your Income, Debt and Interest Rate. You can also see the difference between an amortized loan and interest only loan. You qualify for more with an interest only loan but you’re not paying down your balance.

Here again you can toggle the Debt amount and interest rate of the day to qualify for more or less, note – the amount you qualify for has been reduced by a factor to account for monthly property tax and insurance amounts. This number is more realistic verses not reducing that amount. For complete accuracy, click on ‘Qualify’ and get to the ‘Result’ page and there you can adjust these numbers in the‘Advanced’ area.

(For greater detail about this and other topics, please access our Research page).

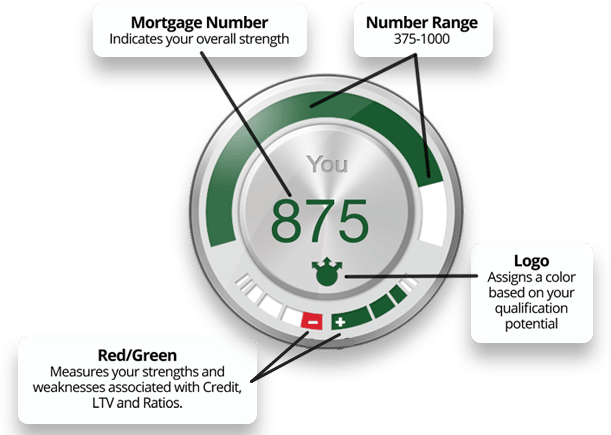

What Your Mortgage Number Means And Why You Need To Know It

Your Mortgage Number illustrates your overall strengths and weaknesses in today’s mortgage environment. To receive your Mortgage Number, simply fill out the Mortgage Number calculator with the details of your financial situation. Once you click the Results button, you get your Mortgage Number.

Mortgage Number is not a credit score, but offers insight on how financial institutions view you as a borrower. Knowing your strengths and weaknesses can be to your advantage when looking for a broker or lender. Knowing how the financial world views you as a borrower can save you time and money. Mortgage Number will get you there for FREE.

How Your Mortgage Number Works Use It To Your Advantage

Once you complete the Mortgage Number calculator, you will receive your Mortgage Number like the one below. With GREEN you qualify. The higher your Mortgage Number, the stronger you are from the lenders perspective. With GRAY, you’re close. And with RED YOUR financial situation needs a little bit of work.

Why Do I Need A Mortgage Number? It's Time to Get Serious

The universal lending system was not designed for the borrower. It includes a complicated qualification process filled with intricate jargon and complex processes. Mortgage Number helps you save the time necessary to scale your goals with clear understanding of opportunities available in the mortgage space.

With Mortgage Number you can be confident that you’re well equipped taking the next steps with a clear understanding of how you fit into today’s lending environment.